- Blog , Digital Transformation

- Published on: 03.04.2025

- 12 mins

Blockchain Technology: How Companies Can Strengthen Their Competitiveness

Modern businesses are already investing in blockchain technology.

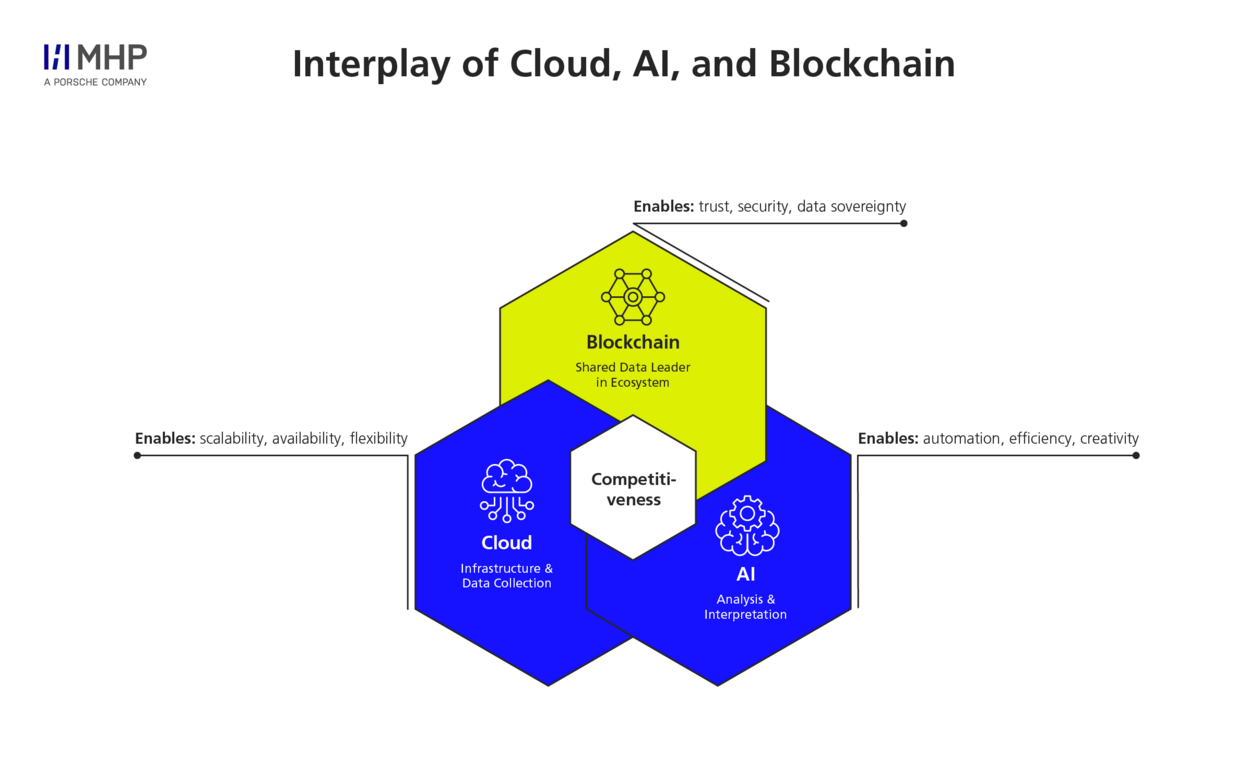

In recent years, innovations such as Generative AI (GenAI) have shown how a technological breakthrough can rapidly transform entire industries and societies. The "ChatGPT moment" illustrates the profound impact of modern digital solutions: seamless process optimization, increased efficiency, and the creation of new jobs are no longer just distant visions but a tangible reality. A similar development is on the horizon for blockchain technology. While blockchain is currently still in the pilot phase (compared to GenAI, which is already scaling), the keyword here is "still." As a relatively new trend, blockchain is on the verge of establishing itself as a critical foundation for numerous digital applications. In the future, alongside AI and cloud technologies, it will play a central role in fostering sustainable business development.

Importantly, blockchain is far more than just the foundation for cryptocurrencies such as bitcoin, a common misconception. The technology can serve as a security layer for AI systems, a foundation for secure digital identities, or a key enabler for efficient data exchange and validation. Major companies such as Siemens with its 'Pebbles' project and initiatives such as Allgäuer Überlandwerk are already demonstrating diverse applications across different industries.

Why Your Company Should Prioritize Blockchain Right Now

Global economic conditions remain volatile. Across industries and regions, companies are under increasing pressure to boost efficiency, drive innovation, and stay competitive in the face of rising costs and complex supply chains. The latest World Competitiveness Index highlights how even advanced economies are struggling to maintain their competitive edge.

This is where blockchain, along with cloud and AI, plays a critical role. With a strategic, demand-driven approach, the technology can help companies strengthen and maintain their competitiveness, even with limited resources. While some are still hesitant, others are already using blockchain to build robust ecosystems that not only address today's challenges, but also lay the foundation for future innovation. The key question is not whether your organization should adopt blockchain, but how quickly you should act to secure your future.

Efficiency, Security, Innovation: The Many Advantages of Blockchain Technology

Blockchain not only optimizes processes but also provides critical competitive advantages in an increasingly digital and globalized economy. Here are the key benefits blockchain technology can bring to your business:

1. Conduct secure and decentralized transactions

Blockchain technology enables secure peer-to-peer transactions without the need for a central intermediary such as a bank or platform operator. Once data is stored on the blockchain, it is easily accessible and cannot be altered. This offers several key benefits:

- Transparency: All transactions are stored in an immutable, publicly available database. Stakeholders can easily track critical steps at any time.

- Immutability: Once recorded, data cannot be tampered with. This increases trust and security for all parties.

- Data sovereignty: You retain full control of your data without relying on a central authority. This independence also reduces costs.

A clear example of these benefits is the "Pebbles" project, a blockchain-based energy trading platform developed by Siemens in collaboration with the regional utility Allgäuer Überlandwerk and the grid operator AllgäuNetz, with support from Kempten University of Applied Sciences and the Fraunhofer Institute for Applied Information Technology. Pebbles focuses on creating a digital platform for regional energy trading, highlighting the business potential of local electricity markets. The blockchain infrastructure enables private energy producers to sell electricity directly to local consumers, bypassing traditional intermediaries. This innovative application demonstrates how blockchain technology can drive greater efficiency, transparency, and trust in the energy sector.

2. Automate processes with smart contracts

Automation brings significant efficiencies and time savings to businesses. In blockchain technology, this is achieved through smart contracts, which are digital agreements that are executed automatically when pre-defined conditions are met. They offer a number of benefits:

- Efficiency: Processes such as payments, deliveries, or contract execution can be automated using smart contracts.

- Cost reduction: Automation saves time and reduces administration.

- Error minimization: Human error is eliminated as contract terms are executed exactly as programmed.

One company taking advantage of these benefits is Bosch with its Decentralized IoT (Internet of Things) initiative. Bosch is using smart contracts on the blockchain to enable autonomous interaction between devices. This allows processes such as maintenance cycles and energy systems to be managed efficiently and securely.

3. Securely manage data with blockchain

As the volume of critical and often confidential digital data increases, so does the risk of attack and manipulation. This makes data security more important than ever. Blockchain offers several advantages in this area:

- Tamper-proof storage: Sensitive data, such as information generated by IoT devices, is protected by the immutable nature of blockchain technology.

- Efficient management: Data is stored and processed in a decentralized manner, reducing potential points of attack and increasing data security.

DHL is a clear example of these benefits. The parcel and mail delivery company is currently investing heavily in blockchain technology for logistics processes and customs clearance. The immutable data structure increases security and trust throughout the supply chain while ensuring transparency and efficiency in complex processes.

4. Invest in tomorrow's technology

Blockchain serves as the foundation for future technologies such as Web3 and regulatory innovations such as eIDAS 2.0.

- Web3: The future of the internet relies on decentralization and user control. Blockchain technology provides the technological foundation to manage digital identities, transactions, and content securely and transparently.

- eIDAS 2.0: With this regulation, the EU plans to provide every citizen with a digital wallet. Blockchain technology can help to store and verify digital identities securely and immutably.

Infobox: What is Web3? Web3 describes the next evolutionary step of the internet, where users are not just consumers but active participants and owners of their data. Blockchain enables this decentralization through transparent and secure networks. Learn more about Web3 in our article: How Web3 Can Contribute to a #BetterTomorrow.

With these benefits, blockchain technology is not just a tool for short-term efficiency improvements but a strategic enabler to prepare your business for the challenges and opportunities of the future.

Blockchain and Artificial Intelligence Working Together

The current hype around GenAI has fundamentally changed the technology sector. As a result, blockchain is also receiving renewed attention. This is because these technologies complement each other perfectly, creating entirely new opportunities for businesses. These include:

- Validation and monetization of AI-generated content: Blockchain can assign immutable tokens to the creative output of GenAI systems, making their origin and authenticity traceable. Non-fungible tokens (NFTs) will also allow artists and businesses to monetize GenAI assets.

- Automation via blockchain-based algorithms: Using smart contracts, blockchain allows AI to perform or verify automated transactions. This increases efficiency and reduces administrative overhead. At the same time, the decentralized structures ensure security and transparency, even across company boundaries.

- Security of AI output: By storing AI-generated content on the blockchain, it becomes immutable and traceable. Organizations benefit from secure data management and, with the right blockchain solution, can restrict sensitive information to authorized users only.

- Trust and transparency with blockchain as a trust layer: For both businesses and end users, trust is a fundamental requirement for adopting new technologies. This is where blockchain and AI complement each other perfectly. While AI enables advanced data analysis and automation, blockchain provides the necessary foundation of trust. With comprehensive documentation and traceability of training data, companies can ensure that AI models are based on ethical and high-quality data. This strengthens business and end-user confidence in AI applications.

Blockchain and AI are two trends that undoubtedly benefit from each other. Together, they can unlock enormous potential. While AI acts as a driver of innovation, blockchain provides the foundation of security and trust to make these innovations sustainable. Companies that recognize and exploit these synergies early on will gain a decisive advantage.

Challenges Companies Face in Adopting Blockchain

As mentioned above, blockchain technology forms a core foundation for Web3. Companies that want to remain competitive in the long term will inevitably need to engage with blockchain. However, as with any innovation, it comes with its own set of challenges.

1. Regulatory uncertainties

One of the biggest hurdles to blockchain adoption is the lack of or unclear legal frameworks in many countries. In particular, compliance with the EU's General Data Protection Regulation (GDPR) raises complex issues for businesses:

- Immutable records: Once data is stored on the blockchain, it cannot be altered or deleted. This potentially conflicts with the GDPR's 'right to be forgotten'.

- Lack of a central point of reference: Since blockchain is organized in a decentralized manner, there is no central authority responsible for data protection issues.

With concepts such as "privacy by design", blockchain applications can be developed to comply with different data protection regulations. The design of the application ensures compliance. The problem lies in the uncertainty and lack of clear regulatory guidance from countries, rather than in the technology itself. With modular blockchain frameworks such as Hyperledger Fabric, privacy-compliant transactions, and data management are already possible today.

2. Technical challenges

The technical challenges of blockchain technology are often questioned in the media. In many cases, there are solutions to these problems. Areas that are repeatedly discussed include scalability, energy consumption, and implementation difficulties.

Scalability

The question of whether blockchain systems can keep up with the speed and high transaction volumes required by modern businesses is often raised. In reality, this is a myth that can be dispelled with the right technologies. Examples abound:

- Polkadot and Cosmos offer scalable, interoperable solutions for cross-sector and cross-company collaborations.

- Polygon and Hyperledger Fabric are highly scalable solutions specifically optimized for enterprise use.

- VeChain has a proven track record in supply chain management, ensuring high efficiency and traceability.

Energy consumption and climate goals

Blockchain is often associated with high energy consumption. However, this perception only applies to technologies such as Bitcoin, which rely on the resource-intensive proof-of-work (PoW) consensus mechanism. Other blockchains use energy-efficient consensus methods such as proof-of-stake (PoS) and others that significantly reduce energy consumption. By choosing the right technology, blockchain initiatives do not pose a challenge to your climate goals.

Outdated IT infrastructures

Many companies are concerned about integrating blockchain into existing systems, especially if these systems are outdated. However, this issue is not specific to blockchain. In general, when a company's level of digitalization is low, the implementation of modern technologies is challenging. Given the competitive market environment, affected companies should act as quickly as possible. In general, blockchain applications can be designed as cloud-based or on-premises solutions:

- Cloud-based applications: Modern, cloud-based infrastructures enable the seamless integration of blockchain applications.

- On-premise solutions: Locally hosted systems can also leverage blockchain, provided there is a solid digital foundation and effective data management in place.

Communication challenges

A frequently underestimated problem in blockchain adoption is the lack of internal understanding of the technology:

- Misunderstandings: There is often a lack of in-depth knowledge about how blockchain works and its benefits. Misinformation in the media exacerbates the problem.

- Internal coordination: These knowledge gaps lead to difficulties in communication and coordination between different departments, which can delay the implementation of blockchain-based solutions.

Organizational effort in the B2B environment

The adoption of blockchain requires close collaboration between business partners, especially in the B2B sector. The organizational effort and alignment required is often a challenge:

- Management: Coordinating projects with multiple partners, including in a consortium, is complex and requires clear responsibilities and careful planning.

- Processes: New technologies often require extensive adjustments to existing processes, which takes time and resources.

Adopting blockchain certainly presents challenges – be they technical, regulatory, or organizational. But with the right strategies and technologies, your organization can overcome these hurdles. Today's blockchain solutions already provide answers to the big questions. Companies that invest early in implementation and adapt the technology to their specific needs will lay the foundation for long-term competitiveness and innovation in the Web3 era.

MHP’s Approaches for a Successful Strategic Implementation of Blockchain Technology

Successful implementation of blockchain technology requires a structured and holistic approach. At MHP, we rely on a comprehensive, three-step, full-circle approach that helps your company to strategically exploit the potential of blockchain, implement the technology in a targeted manner, and scale it successfully in the long term.

Step 1: Analysis – understanding blockchain in the corporate context

The first step is to define the importance of blockchain in the context of your business strategy. Blockchain is not an end in itself, but a tool to increase efficiency and enable innovative business models. MHP dispels myths and analyses the market, competitors, and ecosystems. Interviews with executives and hands-on workshops help to define strategic priorities.

Step 2: Strategic conceptualization and planning – from idea to roadmap

In the second step, we concretize the potential of blockchain technology and lay the foundation for successful implementation. Together, we generate use cases for blockchain, assess technological readiness, and ensure integration into existing processes.

2.1 Analysis of business areas – concretizing potentials

MHP analyzes business areas and processes that could benefit from blockchain. We identify use cases through user research, process analysis, and design thinking workshops, and assess the value of these use cases through business modeling and value chain analysis.

2.2 Ensuring technological and infrastructural readiness

Next, we assess the IT infrastructure and make adjustments where necessary. We use Proof of Concepts (PoCs) to validate the feasibility of the solutions and help you select the appropriate technology (e.g. Hyperledger Fabric or VeChain), system integration, and strategic partnerships.

Step 3: Transform – successful implementation, integration, and rollout

In the third step, we help your organization to implement and scale blockchain solutions. Agile methods allow for flexible adaptation to changes. Phased rollouts minimize risk and create quick wins. Our change management plans foster acceptance within your organization and targeted training prepares employees to work with the new technology. In addition, our strategic partnerships help expand the ecosystem and promote innovative solutions.

With MHP and Innovative Blockchain Technology, Your Company Increases Efficiency, Transparency, and Trust

Blockchain technology has evolved from being the foundation for cryptocurrencies to a key technology for numerous digital applications. It enables secure, efficient, and transparent processes, providing solutions to key challenges such as data security, process automation and fostering innovation. In times of global competition and increasing economic demands, blockchain – in combination with other key technologies – can strengthen your company's competitiveness and ensure long-term sustainability.

With MHP as your strategic partner, you can realize the full potential of blockchain technology. Together, we will implement customized solutions that optimally support your business goals. Take the next step towards a digital future and embrace sustainable innovation now.

FAQ

Blockchain is a digital, decentralized database that stores information in linked blocks. Each block contains data, a timestamp, and a unique code (hash) that makes it secure. Since all participants have a copy of the chain, and new entries can only be added through consensus, blockchain is transparent, tamper-proof, and can be used without central control.

A smart contract is a digital agreement that is automatically executed when pre-defined conditions are met. An example is a maintenance contract for a machine: Once sensors report that a certain number of operating hours have been reached, the smart contract automatically triggers a maintenance request and initiates payment after the maintenance is completed.

Blockchain has a promising future as it improves transparency, security, and efficiency across many industries. Particularly in areas such as supply chain management, finance, and the Internet of Things (IoT), it enables innovative applications and new business models. As technology continues to develop, its relevance will keep growing, extending far beyond cryptocurrencies.